To stay ahead of the competition in the constantly expanding eCommerce industry, SaaS and software developers require a thorough comprehension of the different types of payment processors available. Two frequently used terms in the payment industry are payment aggregator and payment facilitator. Although they share a connection with payment processing, they are certainly not interchangeable.

It is paramount for SaaS and software businesses planning to accept online payments to understand the dissimilarities between payment aggregators and payment facilitators. Let’s dive into the critical differences between payment aggregators and facilitators as well as their potential impact on your payment processing strategy.

Payment Aggregator

What is a Payment Aggregator?

A payment aggregator is a transaction processing service that helps businesses accept payments without requiring them to create their own merchant accounts. It operates as a mediator between the merchant and the acquiring bank, simplifying the system and allowing merchants to process payments through the aggregator's own merchant account.

This makes it easy and convenient for businesses to begin accepting payments without going through a complicated setup process or enduring ongoing maintenance. Payment aggregators often charge a fee for their services, which can be either a percentage of each transaction or a fixed fee per transaction, depending on the agreement accepted between the two parties involved.

How Does It Work?

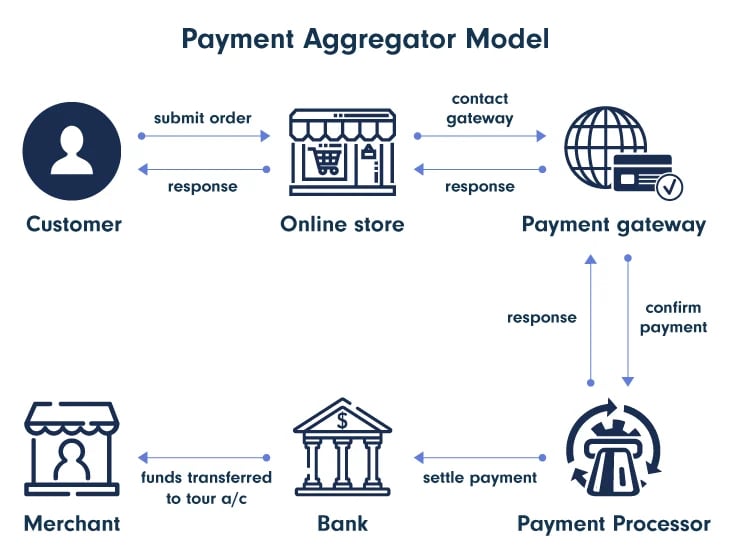

This payment solution acts as an intermediary, enabling the processing of payments between a merchant and an acquiring bank.

Here is what happens behind the scenes:

Step 1: The customer initiates a payment transaction on a merchant's website or mobile app.

Step 2: The payment aggregator securely receives the payment information from the merchant's website or app and forwards it to the acquiring bank for processing.

Step 3: The acquiring bank verifies the payment information and approves or declines the transaction accordingly.

Step 4: The aggregator receives the response from the acquiring bank and communicates it back to the merchant's website or app.

Step 5: If the transaction is approved, the payment aggregator deducts its fee and transfers the remaining funds to the merchant's bank account. It is not done immediately, however. The sub-merchants get funded based on a schedule (monthly, weekly, and so on).

Pros & Cons of Payment Aggregators

When considering whether to use a payment aggregator, companies should carefully consider the benefits and drawbacks of this type of payment solution.

Advantages:

-

- Simple setup: Without a complicated setup procedure and a continuous maintenance process, businesses can start receiving online payments fast and easily.

-

- Many payment alternatives: Customers have additional payment options thanks to payment aggregators, which often accept credit cards, debit cards, local payment methods, and e-wallets.

-

- A cheaper choice for small businesses: This solution frequently charges less expensive transaction fees than a payfac, but generally more than a conventional merchant account provider. This is mainly because they are taking further risk in processing the transactions under their master merchant account, as well as providing ease of use and fast onboarding for the sub-merchants.

- Value-added features: SaaS and software businesses benefit from several additional services like fraud detection, chargeback management, and payment analytics, assisting them in managing their payment processing operations more effectively.

Disadvantages:

-

- Reduced control: As payment aggregators are in charge of the payment processing experience, businesses' ability to influence the checkout procedure and shopper experience is somewhat constrained.

-

- Increased likelihood of account holds: If aggregators suspect fraud or other similar problems, they may be more inclined to put a hold on a company's money, which can interrupt cash flow. This happens because the transactions are processed under the payment aggregator's merchant account.

-

- Restricted customization: Businesses may find it difficult to establish a branded checkout experience due to the limited customization choices that payment aggregators sometimes provide.

- Possibility of account termination: If payment aggregators suspect fraud or other violations of their terms of service, they have the right to terminate a business's account, which can cause a big interruption to business operations.

Key features to consider when choosing a payment aggregator

To ensure this type of payment solution actually fits your business objectives, you should examine these six key factors:

Payment methods: SaaS businesses need a partner that accepts credit cards, debit cards, and e-wallets.

Pricing: Merchants need to be well aware of all the fees involved, from transaction to setup and monthly fees, and decide if these are affordable.

Security: The payment aggregator must protect clients' payment information with SSL encryption and fraud detection.

Customer assistance: If you are looking to provide your clients with dedicated support that resolves concerns quickly, choose a partner that can offer this feature.

Customization: Check if the payment aggregator lets you personalize the checkout experience or add custom fields.

Reports and analytics: Tracking payment analytics to identify improvement areas is crucial, so check if the payment aggregator you are considering offers extensive reporting features.

To ensure a successful partnership, businesses should carefully assess their objectives and priorities when selecting a payment aggregator and examine all of these qualities to guarantee the solution matches their expectations.

Payment Facilitator

What is a Payment Facilitator??

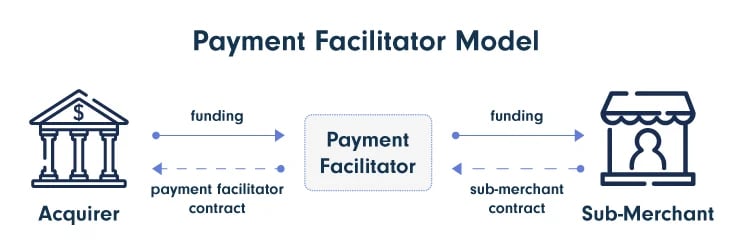

The payment facilitator model offers merchants a turnkey solution to process transactions, allowing them to set up their own merchant accounts and handle operations on their own.

Additionally, merchants can gain access to value-added services like chargeback management and fraud detection. These payment facilitators can frequently offer editable payment pages, enabling retailers to offer branded checkout experiences to customers.

How Does It Work?

This is how they operate:

Step 1: Retailers register with a payment facilitator and give basic company data, like their legal name, tax identification number, and banking information.

Step 2: To ensure that the merchant satisfies the requirements for processing digital payments, the payment facilitator conducts a risk assessment on them. This could very well mean investigating the merchant's legitimacy, past financial transactions and searching for any red flags pointing to fraudulent conduct.

Step 3: The merchant can begin accepting payments using the platform of the payment facilitator after they have been approved. The facilitator gathers transactions from several merchants and deposits them into a single account.

Step 4: After deducting the monthly fee or other costs, the payment facilitator settles the funds into the merchant's bank account, usually on a daily or weekly basis.

This type of payment service partner does more than accept digital payments. It offers merchants access to additional features like chargeback management, fraud detection, reporting, and analytics.

Pros and Cons of using payment facilitator

Like all solutions available to SaaS and software businesses, this option has pros and cons. Understanding them is essential in the process of selecting a strong partner.

Advantages:

-

- Merchant account setup: When collaborating with a payfac, you get your own merchant account, this being the main difference between the two payment providers.

-

- Cost-effective: Unlike conventional merchant account providers, payment facilitators frequently offer competitive pricing and lower costs.

-

- Fraud protection: Payment facilitators frequently provide fraud detection and prevention services, assisting businesses in reducing the risk of chargebacks.

- Customization: These solution providers frequently include editable payment pages and other capabilities, enabling businesses to provide their consumers with a distinctive checkout process.

- Reporting and analytics: Payment facilitators offer thorough reporting and analytics, allowing companies to keep tabs on their payment processing operations and pinpointing areas needing improvement.

Disadvantages:

-

- Limited control: Businesses may have only a limited amount of control over certain operations since payment facilitators administer those processes on the merchant's behalf.

-

- Danger of account holds: If there are suspicions of fraudulent activity, payment facilitators may place holds on a merchant's account, affecting cash flow.

-

- Compliance requirements: Payment facilitators must adhere to stringent compliance standards, which could add a significant workload.

- Transaction restrictions: Companies with a high transaction volume may be affected by the restrictions payment facilitators put on merchants.

- Consumer support: Payment facilitators may not provide thorough customer service, which can be problematic if businesses want help with payment-related problems.

When selecting this type of service provider, businesses should carefully consider their objectives and priorities to make sure the offered solution satisfies their specifications.

Key features to consider when choosing a payment facilitator

Choosing the appropriate payment facilitator is essential for businesses that intend to accept online payments. While choosing a payment facilitator, keep these aspects in mind:

Integration: For a flawless payment processing experience, you’ll want to choose a payment facilitator that easily integrates with your current e-commerce platform, shopping cart, or website.

Security: To guard against fraud and cyberattacks, payment facilitators should have robust security systems in place. Look for solutions that follow industry regulations like PCI DSS (Payment Card Industry Data Security Standard).

Price and fees: To ensure you obtain a competitive rate, compare pricing and fees among various options. To avoid surprises, choose a partner that offers clear pricing and charge structures without any hidden costs or complex pricing schemes.

Responsive Customer Support: For excellent support, you should have access to a full range of support hours, fast response times, and the availability of different communication channels like phone, email, or chat.

Payment options: Check that the payment facilitator accepts card payments, as well as debit cards, e-wallets, and other alternative and local payment options.

Reporting and analytics: Ensure you can track payment processing parameters like transaction volume, chargebacks, and refunds through reporting and analytics systems, allowing you to spot trends and make informed decisions.

Compliance: To guarantee that your operations are legally sound, the payment facilitator should adhere to all applicable laws, rules, and standards, including AML (Anti-Money Laundering) and KYC (Know Your Customer) criteria.

Comparing Payment Services

Differences & Similarities Between Aggregators & Facilitators

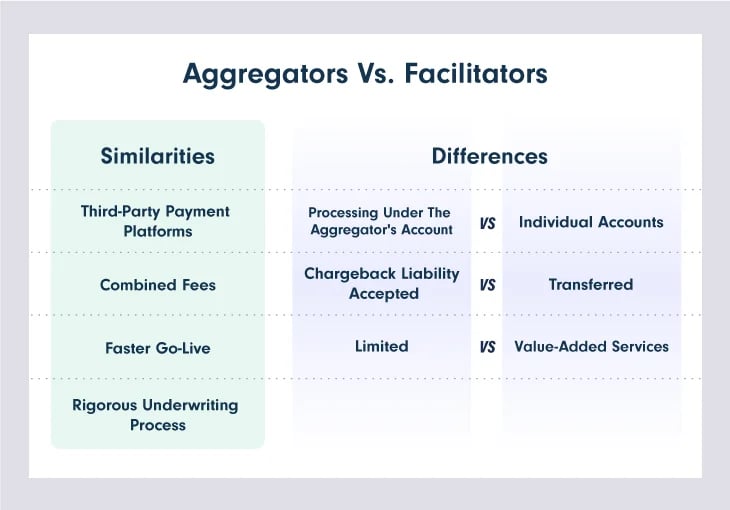

Payment aggregators and payment facilitators are both types of third-party payment processors. Additionally, both payment options will undergo a rigorous underwriting process, during which each merchant is individually vetted and approved before being allowed to use the payment provider's services.

In terms of processing fees, payment aggregators and facilitators generally charge combined fees, made up of setup, transaction, and monthly fees. However, there may be situations where aggregators could charge a flat transaction fee or a percentage of the transaction amount.

While facilitators offer similar benefits to aggregators, there are also notable differences between the two.

One key difference between payment aggregators and facilitators is the status of merchant accounts. Aggregators typically merge multiple merchants under a single master account, while facilitators create separate accounts for each individual merchant.

Regarding liability for chargebacks, payment aggregators are typically responsible for managing these cases and handling any associated fees or fines, though they will usually pass these fees on to the merchant. However, payment facilitators may pass the full responsibilities and fees on to individual merchants directly.

It is also relevant to mention that payment facilitators will provide merchants with several value-added services like fraud detection and prevention, and detailed reporting and analytics tools.

Despite these differences, payment aggregators and facilitators both offer benefits such as simplified payment processing.

In conclusion, businesses should carefully evaluate their specific needs and priorities in the payment process when deciding between solutions.

Which one is better for your business?

Choosing the right payments partner ultimately comes down to understanding your business's unique needs and priorities. If you're a small business or startup with limited resources, a payment aggregator may be a good option for its simplified processing experience and flat transaction fees. However, if you're a larger business with more complex payment processing needs or a high risk of chargebacks, a facilitator may be a better fit due to its greater flexibility, control, and robust fraud prevention and chargeback management services.

Regardless of your choice, carefully evaluate the features, benefits, and pricing models of each option to determine the best fit for your business. By doing so, you can ensure that your payment processing operations are efficient, cost-effective, and tailored to your specific needs, which will, of course, help you reach your bottom-line profits.

No 3rd party integrations. No hidden costs. No wasted time.

Just a solution as unique as your business’s needs.

How Can PayPro Global Help?

PayPro Global is an all-in-one eCommerce solution, providing SaaS, software, and digital product developers with a wide range of features, fast-tracking their global expansion. With PayPro Global's platform, businesses gain streamlined payment processing, worldwide reach, fraud prevention, extension reporting and analytics, customization possibilities, and integration capabilities.

Businesses can benefit from a faster payment processing procedure with our solution. As we support a variety of payment methods and offer personalized, branded checkout experiences, leading to a significant boost in sales. We make it simple for businesses to grow internationally.

To help businesses reduce the risk of chargebacks and secure their revenue, PayPro Global also provides comprehensive fraud detection and prevention services. PayPro Global provides a selection of customization and integration tools to assist developers in integrating the payment processing experience with current systems and customizing it to their particular needs.

Overall, PayPro Global can reduce fraud risk, broaden organizations' global reach, and streamline payment processing operations—all while offering robust reporting and customization options to suit each client's particular requirements.

Final Thoughts

For small enterprises with limited resources or a high volume of low-value transactions, payment aggregators simplify payment processing. Payment facilitators provide more control over payment processes, making them ideal for larger organizations with more complex needs.

Consider your business size, budget, and payment processing demands before selecting a payment solution. Examine payment aggregators' and payment facilitators' features, benefits, and pricing methods to find the best fit for your demands and budget. Take your research further and look into other payment solutions like the Merchant of Record. Perhaps this elaborate business model is a better fit for your needs, fast-tracking your global growth.

Both payment aggregators and facilitators improve online payment processing, worldwide reach, and fraud prevention. Selecting the proper payment model can streamline operations, improve customer experience, and help you reach your business goals.

FAQ

What is the role of a payment gateway in payment aggregation and payment facilitation?

The payment gateway connects merchants and payment processors, making it essential for payment aggregation and facilitation.

It sends merchant payment information to the payment processor for permission and settlement. The payment gateway relays processing fees and transaction data between the aggregator and merchant.

The payment gateway may have to manage various payment processing accounts and configurations because payment facilitators interact with multiple merchants.

How do payment aggregators and payment facilitators make money?

Payment facilitators and aggregators generate revenue by charging a fee for their services related to processing payments. These fees may be in the form of processing fees, transaction fees, or monthly or yearly account fees.

The aggregator often levies a set per transaction fee in addition to a portion of each transaction processed through its platform. Depending on variables like high transaction volumes and the chosen payment method, the percentage fee may change.

The facilitator may additionally levy a comparable transaction fee in addition to extra charges for services like chargeback management, fraud detection, and payment gateway integration. Startup costs, monthly account fees, and other one-time fees may also be imposed by payment facilitators.

Payment facilitators and aggregators may both make money by providing additional value-added services, including currency conversion, recurring invoicing, and subscription management. These services enable businesses to improve their payment processing operations and provide their customers with more flexible payment options.

Can payment aggregator and payment facilitator be used interchangeably?

To be clear, the words "payment aggregator" and "payment facilitator" are not equivalent. Despite the fact that both models permit businesses to accept online payments, they differ in how payments are processed and how much power the merchant is given.

By enabling numerous merchants to process payments through a single account rather than requiring each business to open a separate merchant account, a payment aggregator offers a streamlined payment processing experience. A payment facilitator, on the other hand, gives each individual merchant the ability to create their own merchant account and exercise more control over their payment processing activities.

What is the difference between a payment processor and payment facilitator?

Involvement and responsibility in the processing chain distinguish a payment processor from a payment facilitator. Payment processors help customers and merchants transfer funds. Authorizing, capturing, and settling transactions are their only services to merchants. Payment processors charge a portion of each transaction, usually in the form of a certain percentage.

Payment facilitators offer merchants a complete payment processing solution. They offer turnkey payment solutions to merchants. Payment facilitators enable merchants to open merchant accounts and manage payment processes . The payment facilitator manages risk, fraud, chargebacks, and disputes. Payment facilitators charge transaction, setup, and other fees.

Is PCI compliance necessary for payment aggregation and payment facilitation?

Payment aggregation and facilitation require PCI compliance. All solutions taking card payments must follow the Payment Card Industry Data Security Standard (PCI DSS) to protect cardholder data.

PCI DSS non-compliance can result in fines, reputation damage, and legal action. To secure their clients and businesses, payment aggregators and facilitators must comply with PCI DSS.

Ioana Grigorescu

Ioana Grigorescu is PayPro Global's Content Manager, focused on creating strategic writing pieces for SaaS, B2B, and technology companies. With a background that combines Languages and Translation Studies with Political Sciences, she's skilled in analyzing, creating, and communicating impactful content. She excels at developing content strategies, producing diverse marketing materials, and ensuring content effectiveness. Beyond her work, she enjoys exploring design with Figma.